The Financialization of Renting: From Housing Usage to Financial Flow in the UAE Residential Market

Dubai, UAE

Newsletter 02

EDITORIAL

As we analyze the currents shaping the UAE property market into 2026, a distinct pattern emerges. The market is transitioning from a frontier-style environment toward a more mature, institutionalized ecosystem. Three structural dynamics now form the operating framework of UAE real estate: the financialization of rent, the normalization of pricing, and the deliberate constraint of leverage.

The Financialization of Renting: From Housing Usage to Financial Flow in the UAE Residential Market

Rent as Financial Flow

The headline story is the shift from post-dated cheques to monthly digital payments. However, to view this merely as a “tenant-friendly” convenience is to miss the structural revolution at play.

The integration of platforms like Keyper and the UAE Direct Debit System (UAEDDS) with the Al Etihad Credit Bureau (AECB) transforms rental contracts from simple tenancy agreements into securitized financial products. Rent is no longer just a payment; it is a data point that builds a credit profile.

With the introduction of AECB’s Credit Score 3.0, a tenant’s ability to pay monthly installments is now underpinned by sophisticated risk algorithms, mirroring systems in London or New York. This allows intermediaries to bridge the liquidity gap by paying landlords upfront while collecting monthly payments from tenants - effectively turning lease agreements into tradeable, low-risk debt instruments.

The Anti-Speculation Architecture

Perhaps the most critical “non-event” of the current cycle is that the market has not spiraled into a leverage-fueled bubble. This is by design. The Central Bank’s macroprudential framework, off-plan mortgages capped at 50% LTV, a 40% construction completion rule before financing release, ensures that transaction volume growth is equity-backed, not leverage-driven. For institutional allocators assessing systemic risk, this regulatory architecture is the single most important structural safeguard in the UAE market.

The Bottom Line

The UAE real estate market is no longer defined by acceleration alone, but by structure. Rent is becoming a financial flow, pricing is increasingly standardized, and leverage remains deliberately constrained. In this environment, understanding mechanisms matters more than following momentum.

Sources: AECB Credit Score 3.0 framework; UAE Direct Debit System (UAEDDS); Keyper platform documentation; Dubai Land Department, Smart Rental Index 2025.

The Number That Matters:

~70%

of Dubai residential leasing activity is concentrated in affordable, mid-income segments. Excluding premium, ultra-luxury and trophy assets

What it is:

An estimated 70% of residential leasing activity in Dubai is concentrated in affordable and mid-income, segments. This estimate is derived from segment-level rental market data published in Bayut’s Dubai Rental Market Reports.

What it does not say:

This figure does not imply that luxury or ultra-premium properties are insignificant, nor does it measure the share of total rental value generated by each segment. It is not a headline-driven statistic, but an aggregate view of where day-to-day residential demand is actually expressed.

What it truly reveals:

Despite the media focus on ultra-luxury transactions, the depth and resilience of Dubai’s residential rental market are driven primarily by end-users living, working, and settling in the city. This concentration of activity in non-trophy segments underpins market liquidity, supports absorption, and reinforces the structural role of renting as a core pillar of the UAE’s residential ecosystem.

Source: Bayut Dubai Rental Market Reports (segment-level analysis).

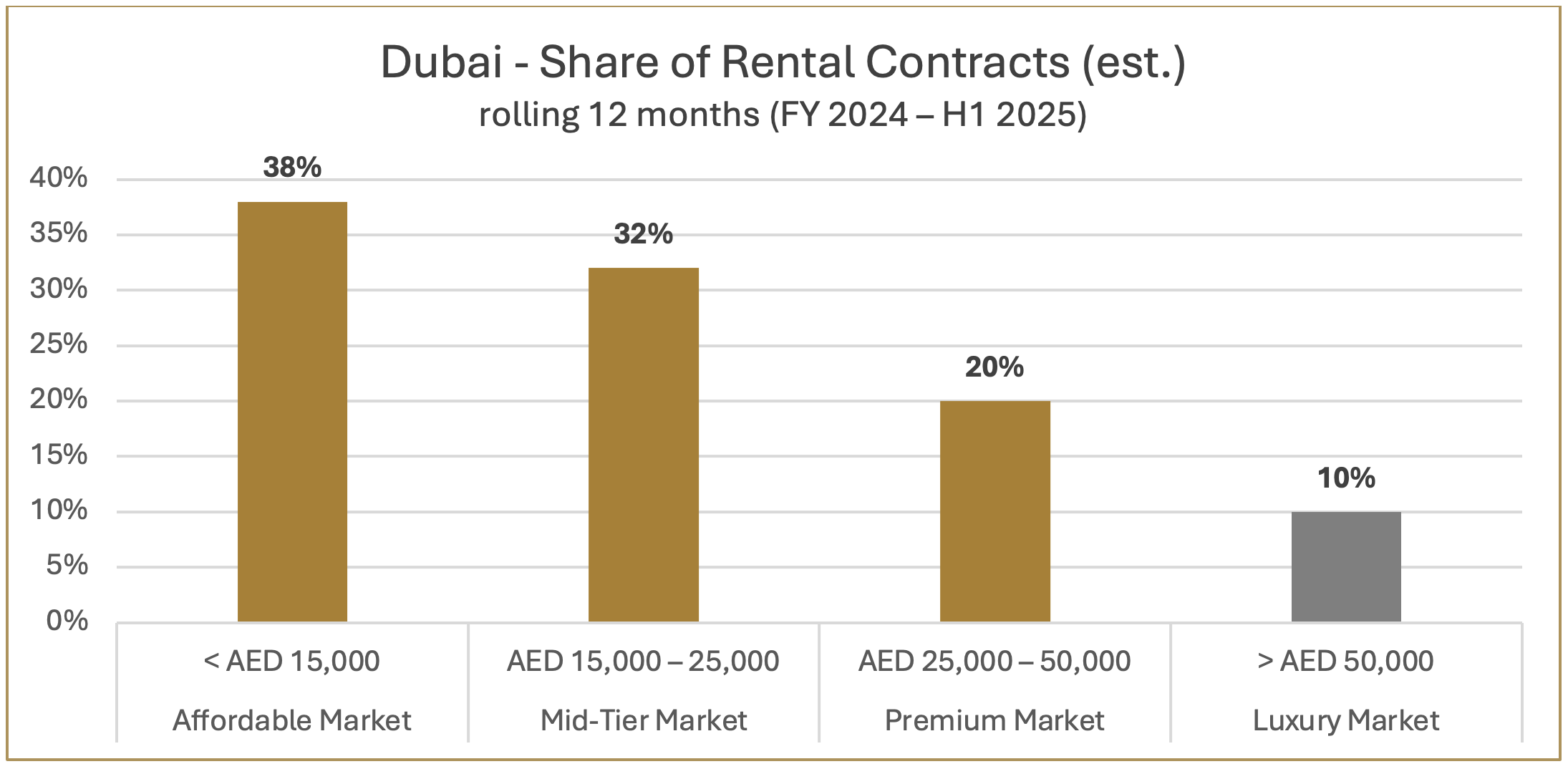

One Chart: Where Rental Market Depth Is Actually Formed

Dubai - Estimated Share of Rental Contracts by Monthly Rent Bracket (rolling 12 months, FY 2024 – H1 2025)

Sources: Bayut Dubai Rental Market Reports (FY 2024–H1 2025); Dubai Land Department (DLD) residential rental registrations; Bread Capital analysis

The End-User Reality

Dubai’s residential rental market is often perceived through the lens of ultra-luxury developments and record-breaking trophy assets. The data tells a different story. The concentration of leasing activity in affordable, mid-income, and premium segments reflects the everyday housing needs of a broad resident base — professionals, families, and long-term expatriates. These segments form the backbone of rental absorption, ensuring liquidity, continuity, and resilience across market cycles.

This end-user dominance creates a structurally stable rental ecosystem in which demand is driven by employment, household formation, and lifestyle needs rather than short-term speculation. In contrast, ultra-luxury assets, although highly visible, constitute a separate sub-market with limited influence on overall rental depth. Understanding this distinction is critical: the true resilience of Dubai’s residential market lies not in headline transactions, but in the scale and consistency of demand generated by those who live and work in the city.

Focus Zone

Downtown Dubai: Prime Density, Global Liquidity and Supply-Constrained Growth

Downtown Dubai

Downtown Dubai functions as the city’s primary urban core, combining high-density residential living with landmark commercial, retail, and cultural infrastructure anchored by Burj Khalifa, Dubai Mall, and Dubai Opera.

Unlike expansion-led submarkets, Downtown Dubai is substantially built out, resulting in structurally constrained supply. The current development pipeline remains limited and targeted, with approximately 7,200 units under construction — primarily premium and branded off-plan projects scheduled for phased delivery between 2026 and 2028.

Residential demand is predominantly usage-driven, supported by employment density, corporate tenancies, and continuous international inflows. While the district attracts global capital and short-term visitors, rental absorption is driven by long-term residents seeking proximity to workplaces, transport connectivity, and lifestyle amenities.

Key Point to Monitor

Asset-level differentiation. In a mature, high-density district, performance dispersion between towers is significant — driven by building age, management quality, and micro-location. Liquidity and resilience are concentrated in a subset of well-positioned assets rather than evenly distributed across the zone.

Conclusion

The UAE has reached a stage of maturity where structural drivers and market depth now function as a single, integrated ecosystem. From the financialization of rent to the demographic weight in Abu Dhabi, the current cycle is driven by a balance of permanent residency and high-volume transient demand. This evolution marks the era of a dual-engine model, where Dubai’s liquidity and Abu Dhabi’s stability together define the region’s new national rhythm.

This publication is provided for informational and educational purposes only. It reflects Bread Capital’s interpretation of publicly available data and market observations and does not constitute investment advice, an offer, or a solicitation.