The Age of Maturity: How the Middle Class Is Reshaping Real Estate in the UAE

Dubai Marina, Dubai, UAE

Newsletter 01

EDITORIAL

The UAE real estate market has reached a defining inflection point. Beyond the headlines, a structural shift toward permanence and nonspeculative demand is redefining the sector. The nation is no longer focused on simply dazzling the world; it is now focused on retaining it.

Our insider reading reveals a dual-engine growth model where Abu Dhabi’s stability and Dubai’s liquidity create a resilient national cycle. Navigating this landscape requires decoding the demographic and regulatory drivers that sit beneath the surface.

The Age of Maturity: How the Middle Class Is Reshaping Real Estate in the UAE

Long perceived as the exclusive playground of ultra-high-net worth individuals and speculative investors, the UAE real estate market is undergoing a profound structural shift in 2025. Beyond the headlines on record-breaking luxury villa transactions, three underlying trends are quietly, but durably, redefining the sector: demographic democratization, rent regulation, and the modernization of payment systems.

The Rise of the Expatriate Middle Class

The profile of expatriation is evolving. While the UAE continues to attract millionaires, the most significant inflow today comes from the middle class, particularly British nationals seeking stability amid economic and fiscal uncertainty in Europe. These new residents are no longer just CEOs, but teachers, healthcare professionals, and tech executives earning between £35,000 and £70,000 per year. This demographic shift is reshaping demand: mid-income buyers (earning AED 20,000 to 40,000 per month) now account for nearly 30% of mortgage applications, with a clear preference for purchasing homes to live in rather than to speculate.

The Affordability Imperative

In response to this influx, policymakers have recognized that the UAE's long-term economic sustainability depends on its ability to house this skilled workforce. Accordingly, Dubai's Crown Prince has approved new policies allocating 1.46 million square meters of land specifically for affordable housing, targeting the development of more than 17,000 units. At the same time, to shield tenants from inflationary pressures, the Dubai Land Department (DLD) rolled out a "Smart Rent Index" in 2025. Powered by artificial intelligence, this tool enhances transparency and curbs arbitrary rent increases, helping stabilize residents' cost of living..

The End of the Cheque Book: Monthly Rent Payments

Finally, 2025 marks the beginning of the end of a long-standing local anachronism: annual or quarterly rent payments by post-dated cheques. A significant reform is now pushing the market toward monthly payments via direct debit or digital platforms. For new contracts signed after January 1, 2026, monthly payments will become the norm, bringing Dubai in line with international standards. Strategic partnerships, such as the one between Property Finder and Keyper, are accelerating this transition and easing cash-flow pressure for tenants, who no longer need to advance large sums upon arrival.

Together, these three dynamics point to a more mature, more stable market, one firmly centered on the end user. The UAE is no longer focused solely on dazzling the world; it is now focused on retaining it.

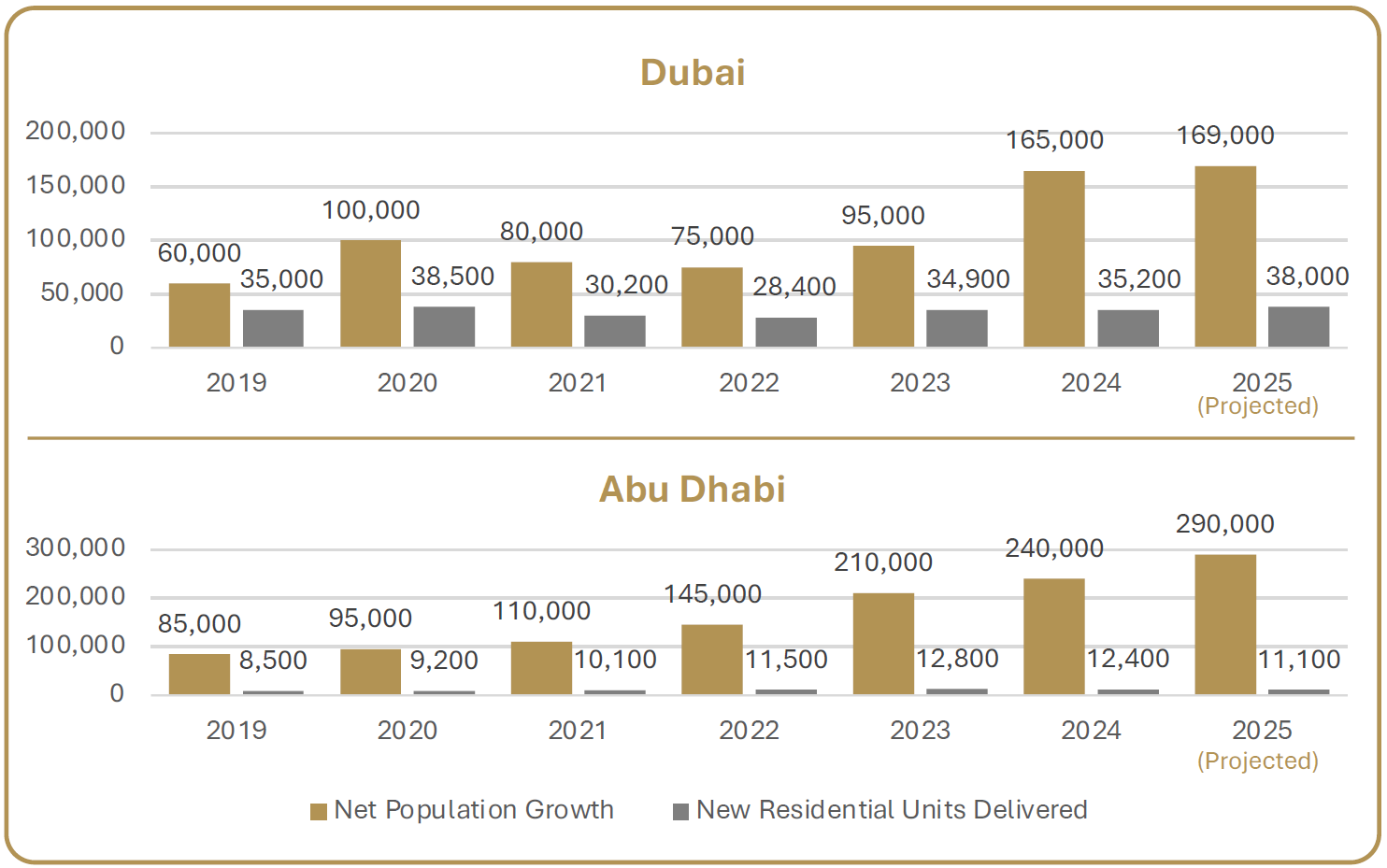

The Number That Matters:

20.4

New Residents/New Home Sold

What it is:

Abu Dhabi’s growth-to-supply ratio for Q3 2025, signifying that for every one new home sold, the population grew by 20.4 new residents.

What it does not say:

This figure does not imply weakness in Dubai’s market, which exhibits a parallel ratio of 4.0, a healthy indicator of demand absorption.

What it truly reveals:

The ratio of 20.4 signals intense, demographically-driven structural pressure on Abu Dhabi’s available housing stock. This is the mathematical expression of a housing shortage fueled by rapid household formation, underpinning the capital’s recent price and rent acceleration.

The Dual-Engine Reality

The UAE residential market is now powered by a permanent structural engine: high population growth. This demographic influx creates a sustainable, non-speculative foundation for housing demand, distinguishing the current cycle from its predecessors.

New household formation is generating robust demand for rental properties and end-user sales, supporting long-term price stability. This domestic strength is further bolstered by massive international traffic, marked by 9.9 million visitors to Dubai in H1 2025, fueling a deep and resilient market for short-term residency.

The market is entering a phase of dual-engine growth. Dubai serves as a high-liquidity international gateway, while Abu Dhabi acts as a stabilizing anchor, driven by significant demographic pressure and government-led strategic investments. Their collaboration is essential for a more balanced and resilient national real estate cycle.

One Chart: Population Growth as the Primary Demand Driver

Sources: Abu Dhabi Statistics Centre, Dubai Statistics, Cavendish Maxwell, REIDIN, Data as of late 2025

Focus Zone

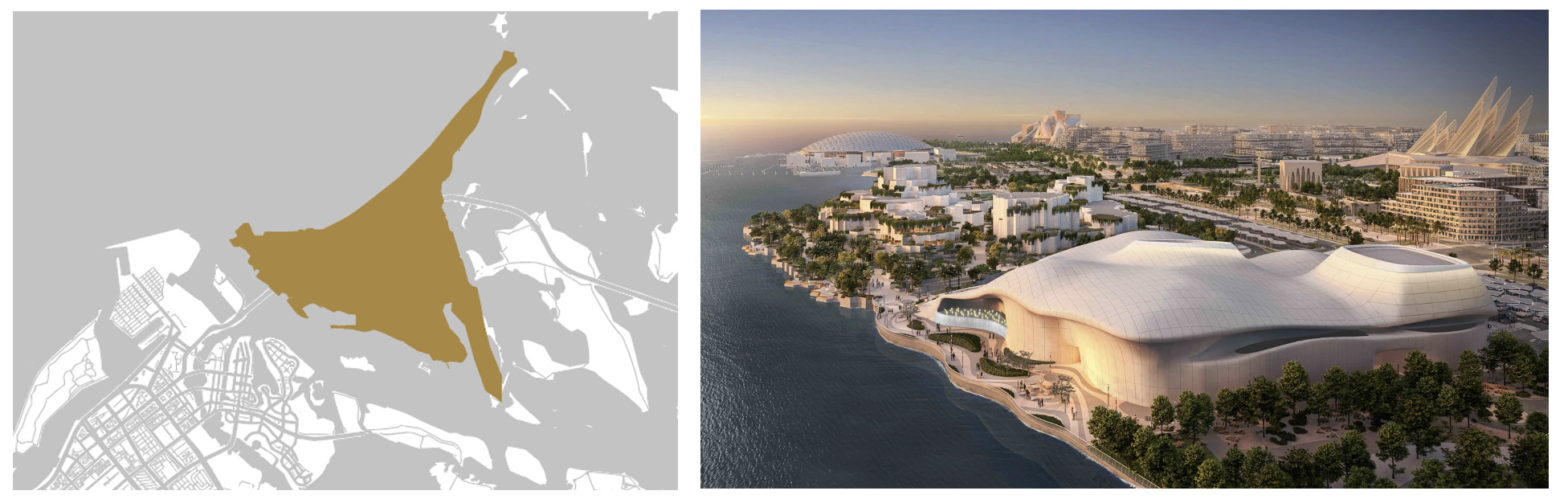

Saadiyat Island, Abu Dhabi: Prime Market, Cultural Hub and Phased Growth

Saadiyat Island, Cultural District.

Saadiyat Island is positioned as a prime residential and cultural district, where long-term lifestyle demand is structurally driven by globally recognized cultural institutions and a controlled development framework.

Saadiyat Island is emerging as a truly unique cultural and residential destination, driven by a long-term vision led by the Government of Abu Dhabi. The island is being developed as a globally distinctive, walkable hub where world-class institutions coexist, including the Louvre Abu Dhabi, the future Guggenheim Abu Dhabi, the Natural History Museum, the Zayed National Museum, TeamLab Phenomena, and the Abrahamic Family House. This exceptional concentration of cultural assets underpins a deliberate strategy to position Saadiyat Island as a global reference for culture, openness, and long-term value creation.

The development pipeline remains significant, with 30+ off-plan residential projects currently underway, scheduled for phased delivery between 2026 and 2030. This supply is being introduced gradually rather than front-loaded.

Demand is predominantly end-user-driven, comprising expatriate professionals, international families, and local high-net-worth residents. Structural demand is reinforced by unique cultural infrastructure and immediate proximity to Abu Dhabi’s urban core.

The key point to monitor remains the absorption capacity of the upcoming premium supply across successive delivery phases.

Market Snapshot

UAE Residential Markets | Dubai & Abu Dhabi – Cumulative Q1–Q3 2025

Transaction Activity & Market Depth

Over the first three quarters of 2025, the UAE residential market continued to operate at historically elevated activity levels, with clear structural differences between Dubai and Abu Dhabi.

Dubai recorded approximately 151 000 residential transactions year-to-date, representing an estimated USD 111 billion in transaction value. Activity remained largely driven by off-plan sales in volume terms, while villas continued to account for a disproportionate share of total value.

Abu Dhabi registered approximately 14 000 residential transactions YTD, with an estimated USD 12.5 billion in transaction value. Market activity remained more concentrated, with transactions clustered in Reem Island, Yas Island and Saadiyat Island, and a higher share of end-user participation.

Observed Price Dynamics

Across both markets, residential prices remained on a positive year-on-year trajectory through Q3 2025. Villas continued to outperform apartments in value growth, while apartment markets showed more moderate, but sustained, appreciation, reflecting differing supply profiles and buyer segmentation.

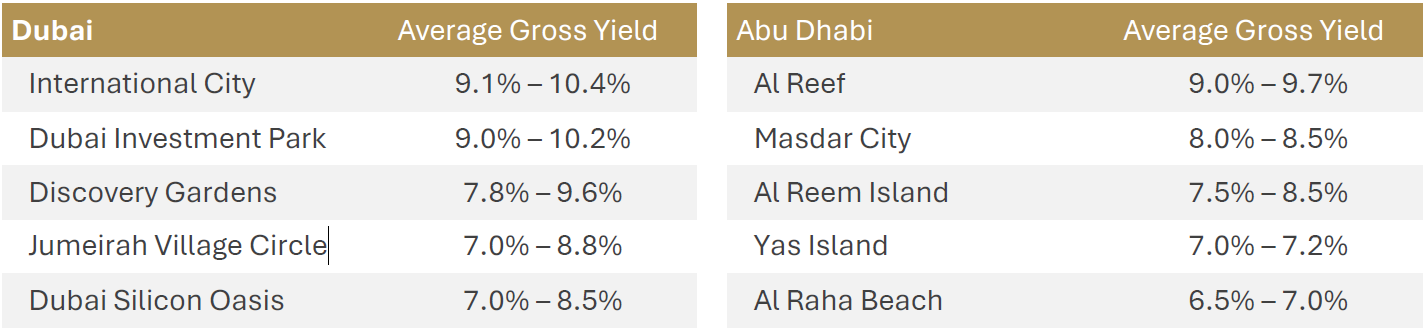

Observed average gross residential yields – Top performing communities for apartments (2025)

Sources: CBRE UAE Real Estate Market Reviews Q1-Q3 2025; Cavendish Maxwell Q3 2025; REIDIN Q3 2025; JLL UAE Residential Q3 2025; Global Property Guide 2025; Bayut Abu Dhabi/Dubai Reports 2025 (H1/Q3); Property Finder UAE Trends 2025; rmax.ae 2025

Reading the divergence

Dubai continues to function as the UAE’s primary liquidity and price-discovery engine, supported by scale and transaction depth. Abu Dhabi, while smaller in absolute terms, reflects a structurally tighter residential market, increasingly shaped by resident fundamentals and phased supply delivery.

Conclusion

The UAE has reached a stage of maturity where structural drivers and market depth now function as a single, integrated ecosystem. From the modernization of payment systems to the demographic weight in Abu Dhabi, the current cycle is driven by a balance of permanent residency and high volume transient demand. This evolution marks the era of a dual-engine model, where Dubai’s liquidity and Abu Dhabi’s stability together define the region’s new national rhythm.

This publication is provided for informational and educational purposes only. It reflects Bread Capital’s interpretation of publicly available data and market observations and does not constitute investment advice, an offer, or a solicitation.